- Private Capital Compass

- Posts

- Private Capital Week in Review 12/5

Private Capital Week in Review 12/5

Welcome to this week’s edition of The Private Capital Compass, brought to you by Private Capital Global (PCG), a Sparc Group company.

In this edition, we examine the shifting dynamics shaping private markets as the industry heads into 2026; from a swelling backlog of aging PE-owned assets to a fundraising environment increasingly dominated by mega-funds. We also spotlight the Bank of England’s landmark stress test of the $16 trillion global private markets ecosystem, the accelerating migration of AI and deep tech companies that is transforming Texas into a premier venture hub, and the escalating cybersecurity vulnerabilities facing family offices amid a surge in AI-driven threats.

This week’s deep dive focuses on the operating realities of private equity ownership, specifically how CEOs can convert heightened pressure, accelerated timelines, and sponsor expectations into disciplined execution and sustained value creation.

The Weekly Shortlist | Stories of the Week

Bank of England Launches Stress Test of Private Equity and Credit | Reuters

Venture Capital Chases Tech to Texas; November Entries Shift Higher | S&P Global

The Growing Cybersecurity Threat For Family Offices | WealthManagament.com

KKR in Talks to Buy Liverpool and PSG Investor Arctos | Financial Times

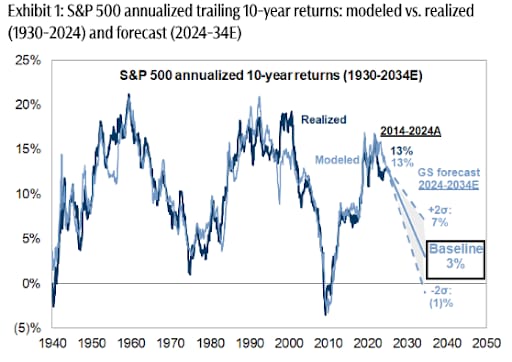

Wall Street Isn’t Warning You, But This Chart Might

Vanguard just projected public markets may return only 5% annually over the next decade. In a 2024 report, Goldman Sachs forecasted the S&P 500 may return just 3% annually for the same time frame—stats that put current valuations in the 7th percentile of history.

Translation? The gains we’ve seen over the past few years might not continue for quite a while.

Meanwhile, another asset class—almost entirely uncorrelated to the S&P 500 historically—has overall outpaced it for decades (1995-2024), according to Masterworks data.

Masterworks lets everyday investors invest in shares of multimillion-dollar artworks by legends like Banksy, Basquiat, and Picasso.

And they’re not just buying. They’re exiting—with net annualized returns like 17.6%, 17.8%, and 21.5% among their 23 sales.*

Wall Street won’t talk about this. But the wealthy already are. Shares in new offerings can sell quickly but…

*Past performance is not indicative of future returns. Important Reg A disclosures: masterworks.com/cd.

Compass Points

Key insights at a glance:

US Private Equity Enters 2026 with Rising Inventory, Slower Realizations, and Increasing Fund Concentration: According to the latest report from Pitchbook, the US private equity market enters 2026 with cautious optimism but faces mounting pressure from an aging portfolio backlog and uneven exit momentum. While exit value and deal flow improved through 2024 and 2025, recovery remains uneven: nearly 13,000 PE-backed companies now sit in inventory, and 30% are seven years or older—signaling extended hold periods and slower monetization across the industry. Cohorts that matured during the downturn, especially 2017 and 2021 vintages, continue to lag historical pacing, underscoring the challenge of clearing accumulated assets. At the same time, capital formation is increasingly consolidating among the largest PE managers, while first-time funds hit record lows. Renewed rate cuts, stabilizing markets, and a gradually reopening IPO window are improving sentiment, but the pace of exits must accelerate materially to relieve pressure. Overall, 2026 is shaping up as a transitional year—marked by improving dealmaking conditions, heightened focus on realizations, and structural shifts that favor scale in fundraising.

Bank of England Launches Landmark Stress Test Targeting Resilience of $16T Private Markets: The Bank of England has launched an unprecedented system-wide stress test examining how the $16 trillion global private equity and private credit markets would respond to a major financial shock, marking the most significant regulatory scrutiny of the asset class to date. With PE-backed companies employing more than two million workers in the UK and private markets now a core financing source for large British corporates, the BoE aims to assess potential spillovers to the broader financial system rather than individual-firm vulnerabilities. Although participation is voluntary, the central bank has secured involvement from firms representing roughly one-third of UK LBO activity and half of all private credit to corporates, including major managers such as Apollo, Blackstone, Bain, Carlyle, CVC, Goldman Sachs, KKR, and Permira. The two-stage test, concluding in early 2027, will model firm-level reactions to stress and potential contagion effects across markets. The initiative follows warnings from Governor Andrew Bailey about rising leverage, opaque structures, and underwriting weakness highlighted by recent US corporate failures.

AI Momentum Accelerates Texas Tech Migration as VC Deployments Approach Record Levels: Venture capital continues to surge into Texas as the state cements its position as the country’s fastest-growing innovation hub, fueled in large part by the migration of AI and deep tech companies from California and other coastal markets. With Texas-headquartered companies attracting $9.9 billion in VC funding through late November, nearly matching last year’s record, the state is benefiting from a powerful combination of lower taxes, business-friendly regulation, scalable labor markets, and an influx of high-profile technology leaders, including Elon Musk–affiliated companies like Tesla, SpaceX, and X.AI. As AI-driven enterprises relocate their headquarters and talent base, VC firms are reallocating capital accordingly, redirecting investment flows toward the Southwest’s expanding tech corridor. The broader private markets landscape mirrors this momentum: global PE/VC deal value surged 31% in November, with AI-related software and electronic equipment seeing outsized activity and sector-defining acquisitions.

Family Offices at High-Risk to New Wave of AI-Driven Cyberattacks: A new Omega Systems survey reveals that family offices are among the least prepared in the financial services sector to defend against rising cyber threats, particularly AI-powered attacks such as deepfakes, impersonation schemes, and sophisticated phishing. Despite managing high-value assets, 67% rely on legacy systems, and only 60% express confidence in their employees’ ability to detect modern cyber threats, significantly below industry norms. Their reluctance to outsource cybersecurity, just 8% use managed service providers, further amplifies their vulnerabilities. With the potential for investor panic, data theft, and operational disruption, the report underscores an urgent need for family offices to upgrade infrastructure, invest in employee training, and adopt advanced cyber defense strategies to keep pace with an increasingly aggressive threat landscape.

Top PE Giants Capture Nearly Half of 2025 Commitments: New PitchBook data shows a sharp consolidation in private equity fundraising, with the 10 largest funds capturing nearly 46% of all U.S. PE capital raised in 2025, up from 34.5% last year, despite an overall market slowdown. Allocators are increasingly directing limited capital to established managers, favoring scale, track record, and operational maturity. The top three funds alone raised $60.4 billion, representing 23.3% of all commitments year-to-date. Meanwhile, emerging managers face growing headwinds: only 41 first-time funds have closed in 2025, the lowest on record, as firms with more than 10 fund vintages secured 61% of total capital raised. With fundraising down to $259 billion year-to-date from $372.6 billion in 2024, the data signals a decisive “flight to experience”—solidifying advantages for mega-funds and increasing barriers for new entrants across the private equity landscape.

Deal Spotlight: KKR in Talks to Acquire Majority Stake in Arctos Partners

Transaction: US private capital giant KKR is reportedly in advanced discussions to acquire a majority stake in Arctos Partners, a leading investor in professional sports franchises globally. With more than $700 billion AUM, KKR is evaluating Arctos as a strategic platform that aligns with its long-term expansion into products appealing to both institutional and retail investors. Founded in 2019, Arctos has quickly become a central player in the institutionalization of sports investing, holding minority stakes in premier global franchises, including Liverpool FC, Paris Saint-Germain, the Golden State Warriors, Los Angeles Dodgers, Utah Jazz, Buffalo Bills, and the Aston Martin Formula 1 team.

Why It Matters: The deal underscores the accelerating maturation of the secondaries market. Limited partners are increasingly using secondaries to manage liquidity, rebalance portfolios, and navigate longer fund durations. At the same time, GPs are leveraging continuation funds and structured solutions at record levels. Arctos’s deep expertise in secondaries would offer KKR immediate scale and technical capability in a segment projected to continue outgrowing traditional fundraising. This move signals that major platforms view secondaries not as a niche strategy but as a core component of the private capital ecosystem for the coming decade.

KKR’s pursuit of Arctos demonstrates the expansion of private equity into global sports; a sector once dominated by individual billionaires and now characterized by institutional ownership, improved governance, and professionalized commercial operations. Sports assets have shown strong inflation-linked revenue growth, resilient global demand, and increasing monetization of media rights, international merchandising, and digital fan engagement.

If completed, the KKR–Arctos deal would mark a defining moment in the evolution of sports investment, signaling that blue-chip private equity firms now view sports not merely as an opportunistic play but as a foundational pillar in long-term capital strategy.

Deep Dive:How CEOs Turn Pressure into Performance

Private equity ownership introduces a fundamentally different operating environment for management teams. Expectations are higher, timelines are compressed, and the path to value creation becomes the central organizing principle of the company’s strategy. Below is a deeper look at the core elements that enable executives to thrive under PE ownership and deliver meaningful value creation.

1. Build the Value Creation Blueprint

The first 90 days under private equity ownership are decisive. During this window, CEOs must collaborate with the sponsor to develop a fact-based, actionable Value Creation Plan (VCP) that anchors all future decision-making. Great CEOs work with Operating Partners and the deal team to:

Build a deep fact base on performance drivers, market dynamics, and operating constraints

Identify three to five value creation levers capable of doubling enterprise value or generating a 3x+ MOIC

Establish KPIs that measure progress in real time

Communicate a clear, unified vision that cascades through the organization

2. Operate with Transparency

Once the VCP is set, the CEO–sponsor relationship must be built on radical transparency. PE firms are highly data-driven and deeply invested in the success of the plan. What they cannot tolerate is opacity. Leaders who thrive under PE ownership:

Maintain a consistent communication cadence

Share risks and challenges early—with solutions, not excuses

Provide timely performance updates with context, not just numbers

Encourage open, two-way dialogue with board members and Operating Partners

3. Discipline, Tempo, and Accountability

Private equity companies operate at a different metabolic rate. The tempo is higher, decisions are faster, and execution is non-negotiable. To manage this environment effectively:

Define clear operating priorities around the VCP

Establish dashboards linked to KPIs

Set strong project management mechanisms to monitor initiatives

Assign a primary liaison (often the CFO) to centralize communication with the sponsor

This discipline protects the organization from unnecessary distractions and ensures that every team member understands how their work ties to value creation. Private equity is not merely about working harder, it’s about creating a repeatable operating cadence that eliminates drift and drives measurable results.

4. Build the A-Team Required for Value Creation

No value creation plan can be executed without the right team. PE-backed transformations regularly require leadership changes, not out of preference, but out of necessity. High-performing CEOs are honest about talent gaps and unafraid to make early moves. This includes:

Assessing capabilities against the VCP

Replacing underperformers quickly

Recruiting leaders with transformation experience

Establishing a culture of accountability and ownership

PE sponsors consistently cite talent quality as the number one driver of returns. CEOs who build an A-team accelerate value creation. Those who hesitate signal misalignment.

5. Leverage the PE Ecosystem

Today’s private equity firms bring extensive resources: Operating Partners, functional experts, industry specialists, and peer forums. CEOs who treat these assets as extensions of the management team unlock faster insights and avoid common execution pitfalls. The most successful leaders actively engage this ecosystem for:

Operating model design

Pricing and GTM acceleration

Procurement and cost initiatives

M&A integration

Digital and data transformation

6. Tailor the Operating Model to the Investor

Not all PE firms operate the same way. Some are hands-on and operationally embedded; others are strategic and decentralized. Successful CEOs invest time upfront in understanding:

How their sponsor makes decisions

The cadence and expectations of the board

Which Operating Partners hold influence

The firm’s communication preferences

How they measure performance against the VCP

This insight allows CEOs to calibrate their leadership approach and avoid misalignment before it becomes detrimental.

Compass Call: Lead with Intent

Private equity ownership is a totally new operating model. Expectations rise, timelines compress, and the path to value creation becomes the definitive measure of leadership. For CEOs and operators entering this environment: align quickly, operate transparently, and execute with discipline.

The leaders who excel establish clarity and vision early on. They build tight communication rhythms, elevate the operating cadence, and surround themselves with talent capable of delivering against the investment thesis. And most importantly, they lean into the partnership with their sponsor, using the full operating ecosystem to accelerate performance.

If your organization is entering a new phase of private equity ownership, or preparing for one, now is the time to strengthen your leadership playbook. Reassess your value creation plan. Pressure-test your KPI framework. Reevaluate your talent bench. Build the operating muscle required to move at PE speed.

Thank you for joining us for this week’s edition of The Private Capital Compass. As we look toward 2026, we’re energized by the momentum building across the Private Capital Global community and the events ahead in Austin, Boston, Chicago, London, New York, and San Francisco.

For deeper perspectives throughout the year, be sure to subscribe to The Private Capital Insiders Podcast, hosted by Frank Scarpelli, where leading dealmakers and operators share firsthand insights on today’s evolving private capital landscape.

Our commitment remains unchanged: to keep you informed, connected, and equipped with the analysis and intelligence you need to convert market insight into actionable value across your investments and portfolio companies.

Opening & Closing Remarks from Erik Boender, Vice President & COO, Private Capital Global (a Sparc Group company)

Did you enjoy today's newsletter?We are constantly looking to improve our content output. Please take a quick second to let us know what you thought. |

Reply